Tools

Concepts

Deming Profound Knowledge & Systems Thinking

Deming on Management of People

Applications

Difference between TQM and Six Sigma

Importance of SPC to Quality Management System Performance

Cost of Quality Overview

An excerpt from The Handbook for Quality Management (2013, McGraw-Hill) by Paul Keller and Thomas Pyzdek

The history of evaluating the cost of quality (sometimes referred to as the cost of poor quality) dates to the first edition of Juran's QC Handbook in 1951. Today, quality cost accounting systems are part of every modern organization's quality improvement strategy. Indeed, quality cost accounting and reporting are part of many quality standards. Quality cost systems help management plan for quality improvement by identifying opportunities for greatest return on investment. However, the quality manager should keep in mind that quality costs address only half of the quality equation. The quality equation states that quality consists of doing the right things and not doing the wrong things. Doing the right things implies developing product and service features that satisfy or delight the customer. Not doing the wrong things means avoiding defects and other behaviors that cause customer dissatisfaction. Quality costs address only the latter aspect of quality. It is conceivable that a firm could drive quality costs to zero and still go out of business.

The fundamental principle of the cost of quality is that any cost that would not have been expended if quality were perfect is a cost of quality. This includes such obvious costs as scrap and rework, but it also includes many cost of quality categories that are far less obvious, such as the cost of reordering to replace defective material. Service businesses also incur quality costs; for example, a hotel incurs a quality cost when room service delivers a missing item to a guest. Specifically, quality costs are a measure of the cost of quality categories specifically associated with the achievement or non-achievement of product or service quality, including all product or service requirements established by the company and its contracts with customers and society. Requirements include marketing specifications, end-product and process specifications, purchase orders, engineering drawings, company procedures, operating instructions, professional or industry standards, government regulations, and any other document or customer needs that can affect the definition of product or service. More specifically, quality costs are the total of the cost incurred by (a) investing in the prevention of non-conformances to requirements, (b) appraising a product or service for conformance to requirements, and (c) failure to meet requirements (see Fig. 8.1).

PREVENTION COSTS

The costs of all activities specifically designed to prevent poor quality in products or services. Examples are the costs of new product review, quality planning, supplier capability surveys, process capability evaluations, quality improvement team meetings, quality improvement projects, quality education and training.

APPRAISAL COSTS

The costs associated with measuring, evaluating or auditing products or services to assure conformance to quality standards and performance requirements. These include the costs of incoming and source inspection/test of purchased material; in process and final inspection/test; product, process, or service audits; calibration of measuring and test equipment; and the costs of associated supplies and materials.

FAILURE COSTS

The costs resulting from products or services not conforming to requirements or customer/user needs. Failure costs are divided into internal and external failure cost categories.

INTERNAL FAILURE COSTS

Failure costs occurring prior to delivery or shipment of the product, or the furnishing of a service, to the customer. Examples are the costs of scrap, rework, re-inspection, retesting, material review, and down grading.

EXTERNAL FAILURE COSTS

Failure costs occurring after delivery or shipment of the product, and during or after furnishing of a service, to the customer. Examples are the costs of processing customer complaints, customer returns, warranty claims, and product recalls.

TOTAL QUALITY COSTS

The sum of the above costs. It represents the difference between the actual cost of a product or service, and what the reduced cost would be if there was no possibility of substandard service, failure of products, or defects in their manufacture.

Figure 8.1. Quality costs general description (Campanella, 1990 by permission).

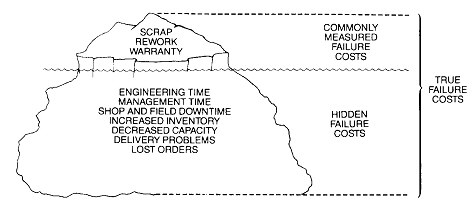

For most organizations, quality costs are hidden costs. Unless specific quality cost identification efforts have been undertaken, few accounting systems include provision for identifying quality costs. Because of this, unmeasured quality costs tend to increase. Poor quality impacts companies in two ways: higher cost and lower customer satisfaction. The lower satisfaction creates price pressure and lost sales, which results in lower revenues. The combination of higher cost and lower revenues eventually brings a crisis that may threaten the very existence of the company. Rigorous cost of quality measurement is one technique for preventing such a crisis from occurring. Fig. 8.2 illustrates the hidden cost concept.

Figure 8.2. Hidden cost of quality and the multiplier effect. From Principles of Quality Costs, 2nd Edition p. 11, Jack Campanella, Editor. Copyright © 1990 by ASQ Quality Press.

See also:

Strategy for Reducing Quality Costs

Benefits of Quality Cost Reduction

The Handbook for Quality Management

Online Quality Management Study Guide

Learn more about the Quality Management tools for process excellence in The Handbook for Quality Management (2013, McGraw-Hill) by Paul Keller and Thomas Pyzdek or their online Quality Management Study Guide.